Key messages

- Uranium and thorium are naturally occurring elements that are widespread in the Earth's crust. Mining occurs in locations where such elements are naturally concentrated.

- To make nuclear fuel from uranium ore, the uranium is extracted from the host rock and then the 235U isotope is progressively enriched.

- Australia has the world’s largest Economic Demonstrated Resources of uranium and is the world’s third largest uranium producer.

- Australia’s average annual export volume of uranium for the last 10 years is approximately 6,048 tonnes (tU). However, this will drop by approximately 1,900 tU p.a. (30 per cent) in the short to medium term as the Ranger mine ceased operations in January 2021.

- Thorium has been used previously in the nuclear generation process but its use is still largely experimental and there is no current commercial market for thorium.

- Thorium is not produced in Australia and production on a large scale is unlikely in the next few decades.

Summary

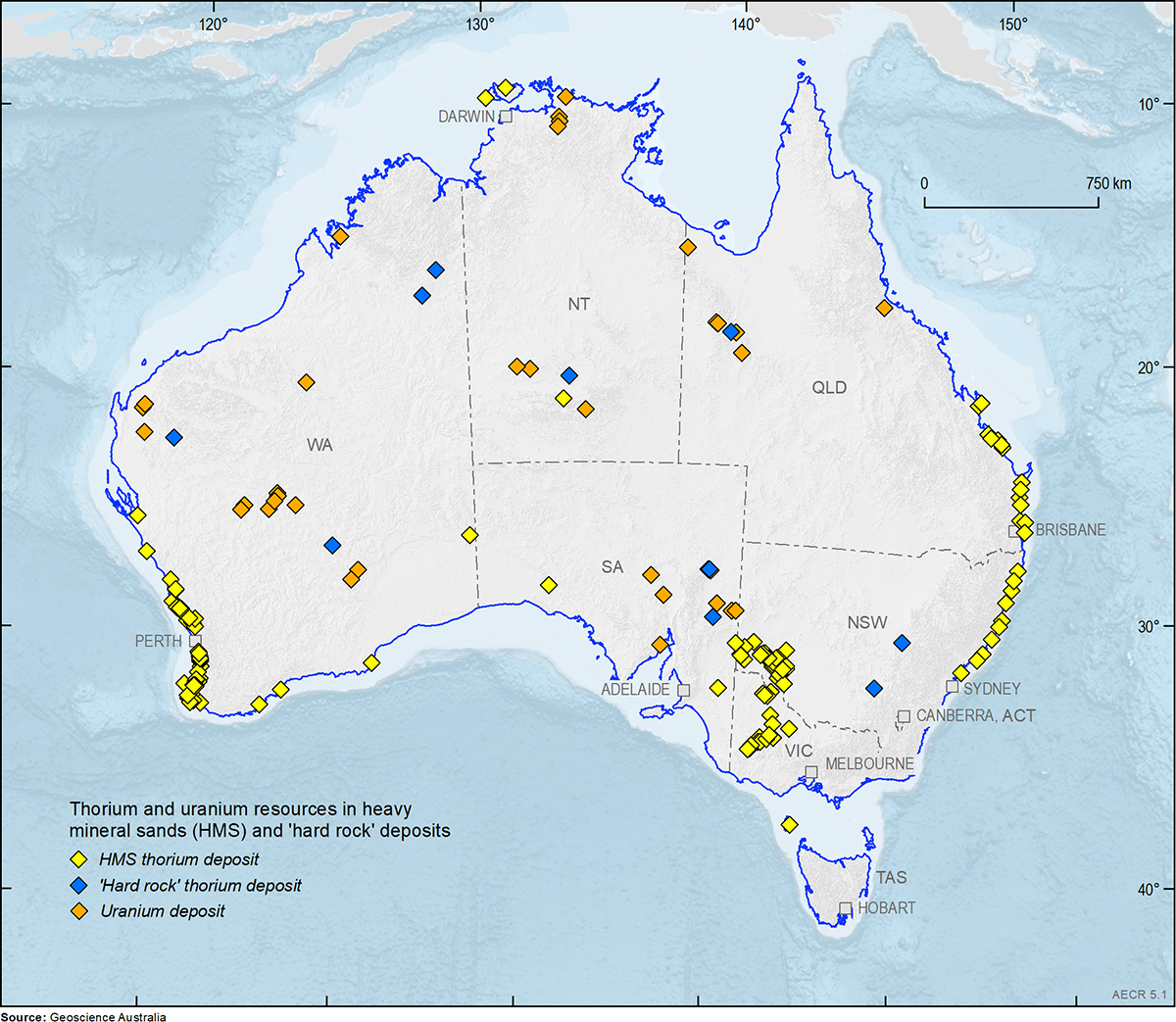

Australia has widespread uranium- and thorium-bearing mineral deposits (Figure 1). The Olympic Dam mine in South Australia is the world’s largest deposit of uranium.

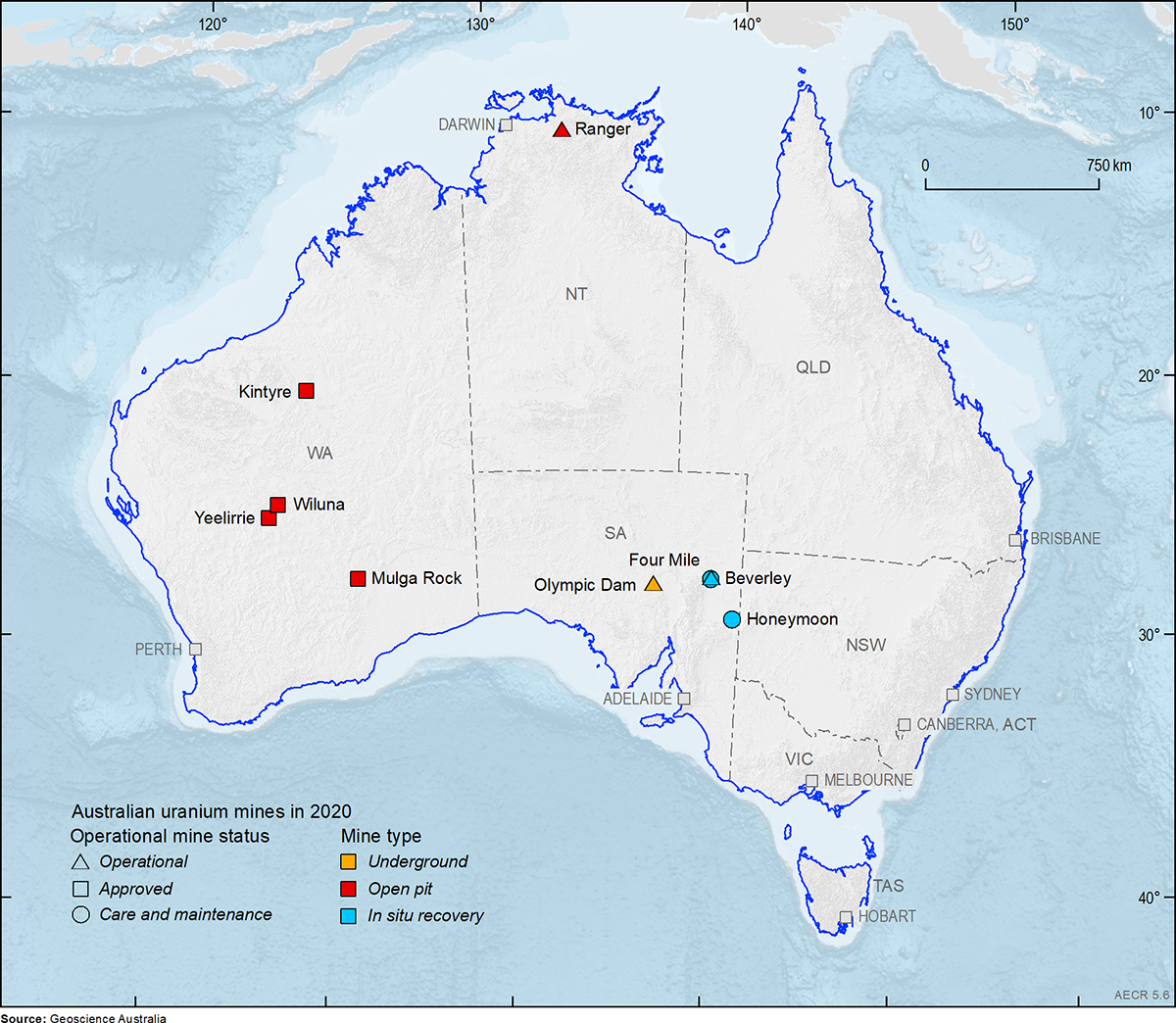

Australia has the world’s largest Economic Demonstrated Resources (EDR) of uranium—1,147 thousand tonnes of uranium (ktU; 642,491 petajoules [PJ]) as at 31 December 2019—and is the world’s third largest producer of uranium. In 2019, Australia had three producing uranium mines: Olympic Dam and Four Mile in South Australia, and Ranger in the Northern Territory.

Australian uranium supply has declined moderately over the past ten years, mainly due to the closure of two mines in 2014 and 2015. In the short to medium term, due to the closure of the Ranger Mine in January 2021, Australian production of uranium will decrease by approximately 1,900 tU p.a. Australia’s uranium exploration expenditure has been in decline since the crash of the uranium price in 2011, following the Fukushima Daiichi nuclear accident. Additionally, bans and uncertainties concerning uranium mining in some states negatively affect Australia’s ability to attract uranium exploration investment. In 2019 exploration investment was $10.2 million, a fall of 17 per cent compared with the previous year and the lowest it has been since 2003.

There are currently no commercial applications for thorium and world production and consumption rates are negligible. As such, thorium is not produced in Australia and production on a large scale is unlikely in the next few decades.

At present, Australia has no plans for a domestic nuclear power industry. However, interest in the industry at state level led to the South Australian Nuclear Fuel Cycle Royal Commission in 2015 and, more recently, the New South Wales Uranium Mining and Nuclear Facilities (Prohibitions) repeal Bill 2019 and the Victorian Inquiry into Nuclear Energy Prohibition (2020). Additionally, at the federal level, an Inquiry into the Prerequisites for Nuclear Energy in Australia by the House of Representatives Standing Committee on the Environment and Energy was undertaken 2019.

Australia’s identified resources

Uranium

Uranium is a mildly radioactive element that is widespread at levels of 1–4 parts per million (ppm) in the Earth’s crust. Concentrations of uranium-rich minerals, such as uraninite, carnotite and brannerite, can form economically recoverable deposits. The majority of Australia's uranium occurs in four main types of deposit: iron oxide breccia complexes, unconformity-related resources, sandstone resources and palaeochannel/calcrete-style resources.

Once mined, uranium is processed into uranium oxide (U3O8), also referred to as uranium oxide concentrate, and is exported in this form. Natural uranium (from mine production) contains approximately 0.7 per cent of the uranium isotope 235U and 99.3 per cent 238U.

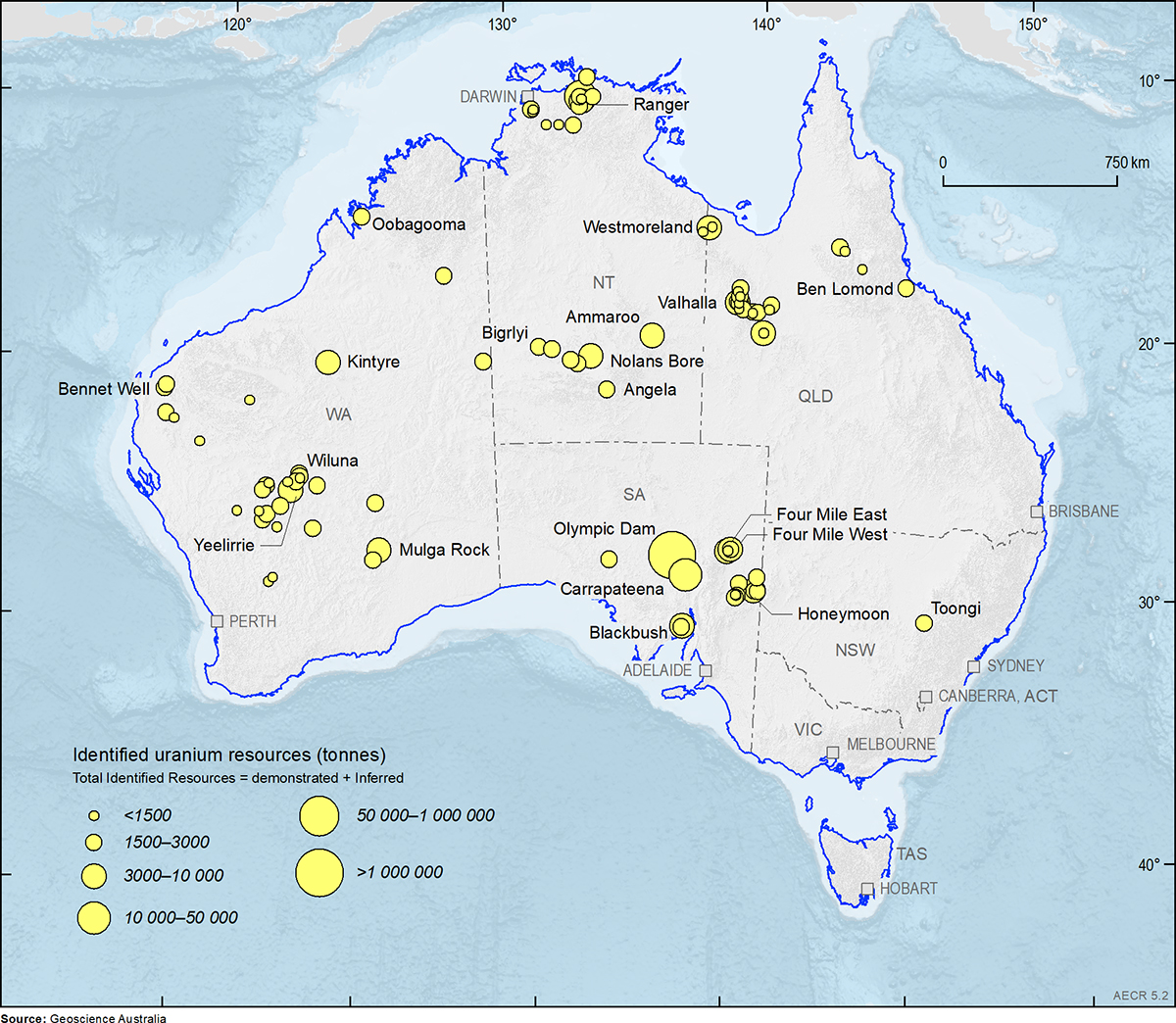

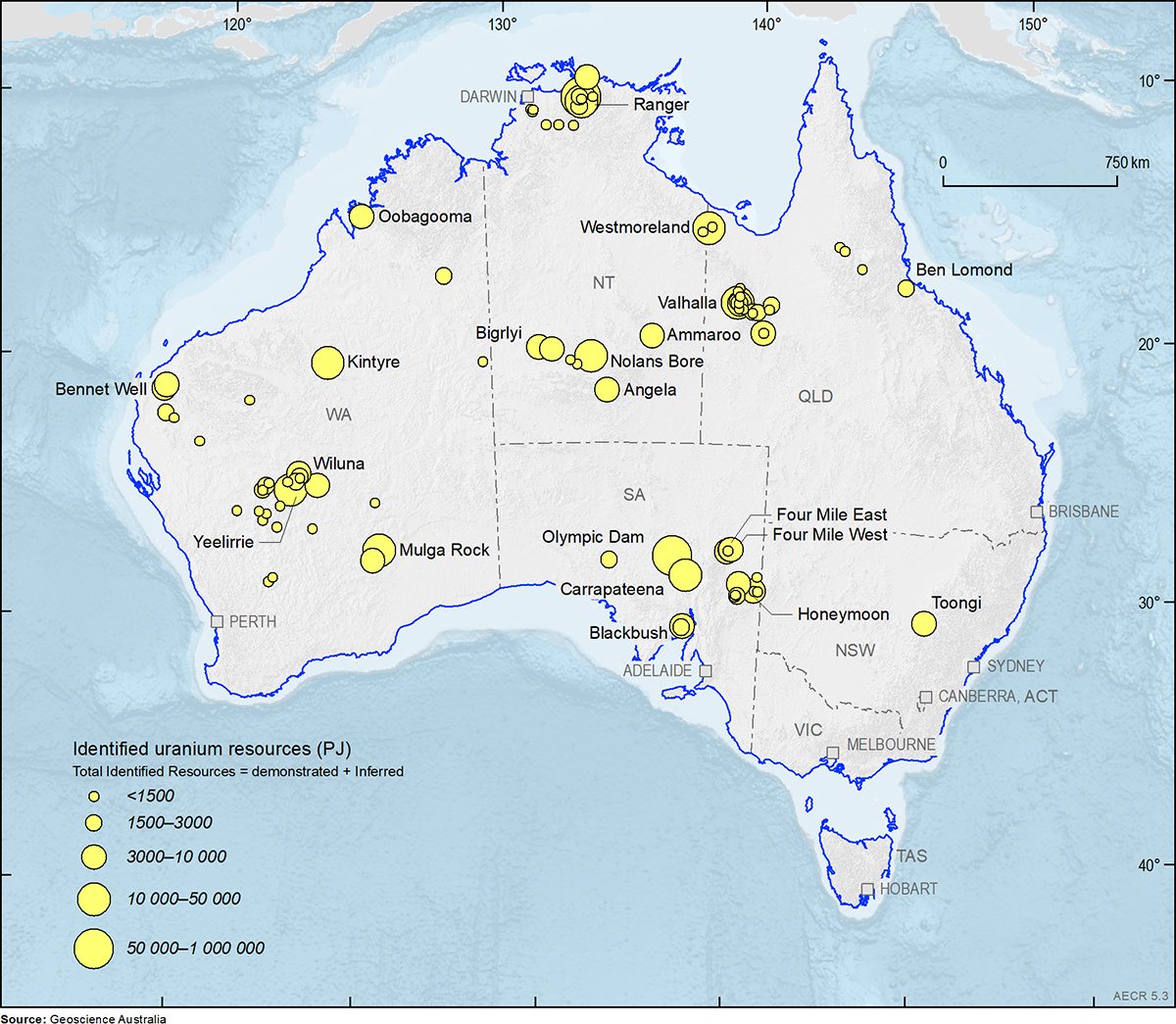

As at December 2019, Australia’s EDR for uranium was 1,147 ktU (642,491 PJ). An additional 56 ktU (31,300 PJ) was classified as Subeconomic Demonstrated Resources and 722 ktU (404,400 PJ) as Inferred Resources. Australia’s total Identified Resources were 1,952 ktU (1,093,400 PJ). Although most Australian states and territories host uranium deposits, EDR are concentrated in South Australia, the Northern Territory and Western Australia (Figure 2 and Figure 3). South Australia’s Olympic Dam is the world’s largest uranium deposit, with an EDR of 876 ktU (490, 371 PJ).

Thorium

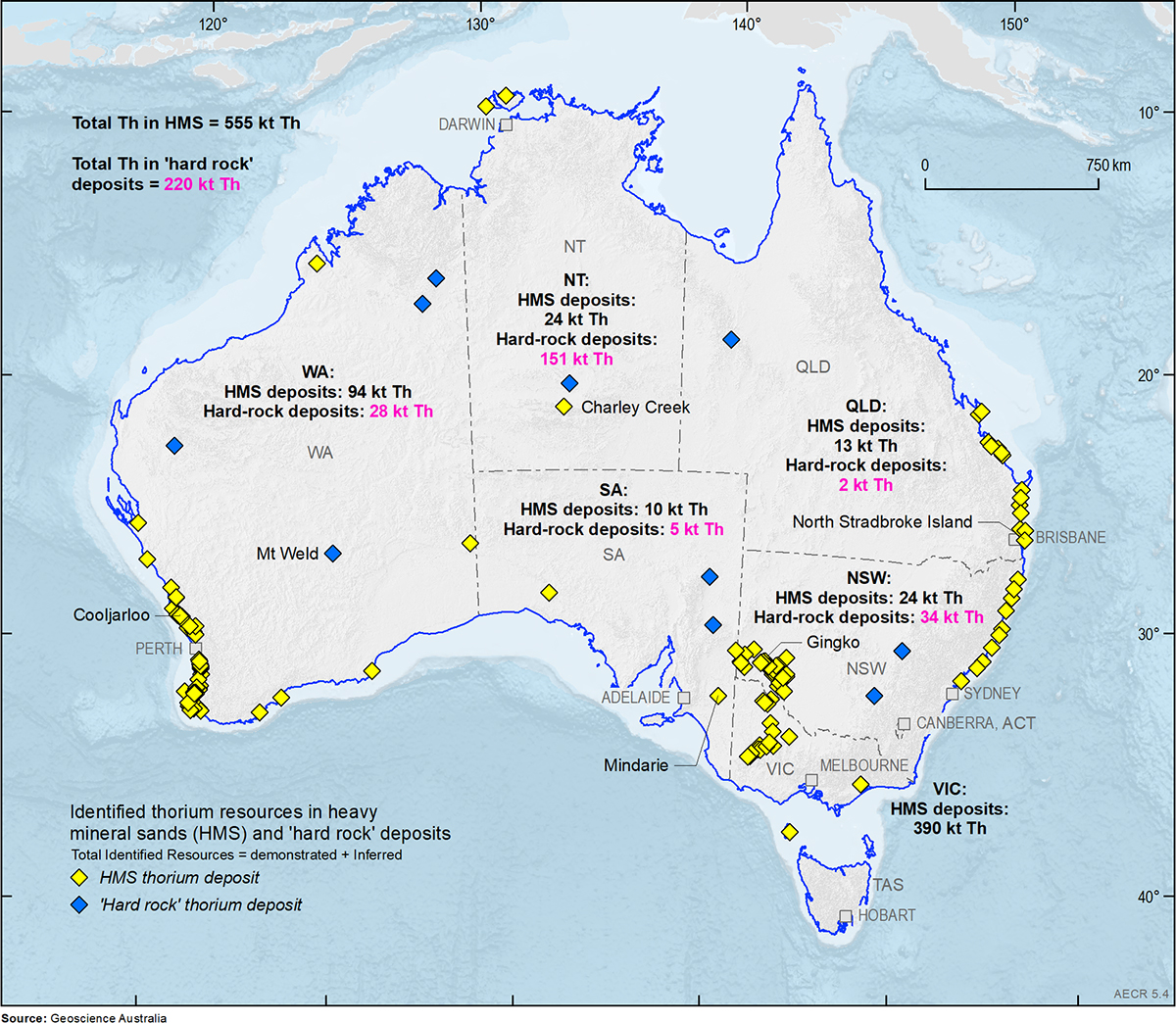

Thorium is a naturally occurring slightly radioactive metal that is three to five times more abundant in the Earth’s crust than uranium. It is less conducive to nuclear weapons proliferation and, due to its greater energy-producing efficiency, generates substantially less radioactive waste. The most common source of thorium is monazite, a rare earth phosphate mineral that is a minor constituent of heavy mineral sand (HMS) deposits. On average, monazite contains approximately 6 per cent thorium and 60 per cent rare earth elements.

In Australia, approximately 80 per cent of thorium resources are contained in HMS deposits; the remaining 20 per cent are in rare earth element hard-rock deposits (Figure 4). Monazite and thorium resources are not generally published and so Geoscience Australia estimates the monazite (and hence thorium) content in deposits and classifies these estimated resources as Inferred Resources. Using this approach, Geoscience Australia estimates that Australia’s total identified in situ thorium resources were approximately 1,265 kt as of 31 December 2019.

Currently, no thorium is produced in Australia. Although HMS deposits containing monazite are currently being mined, the monazite is not recovered due to the lack of a thorium market.

Production

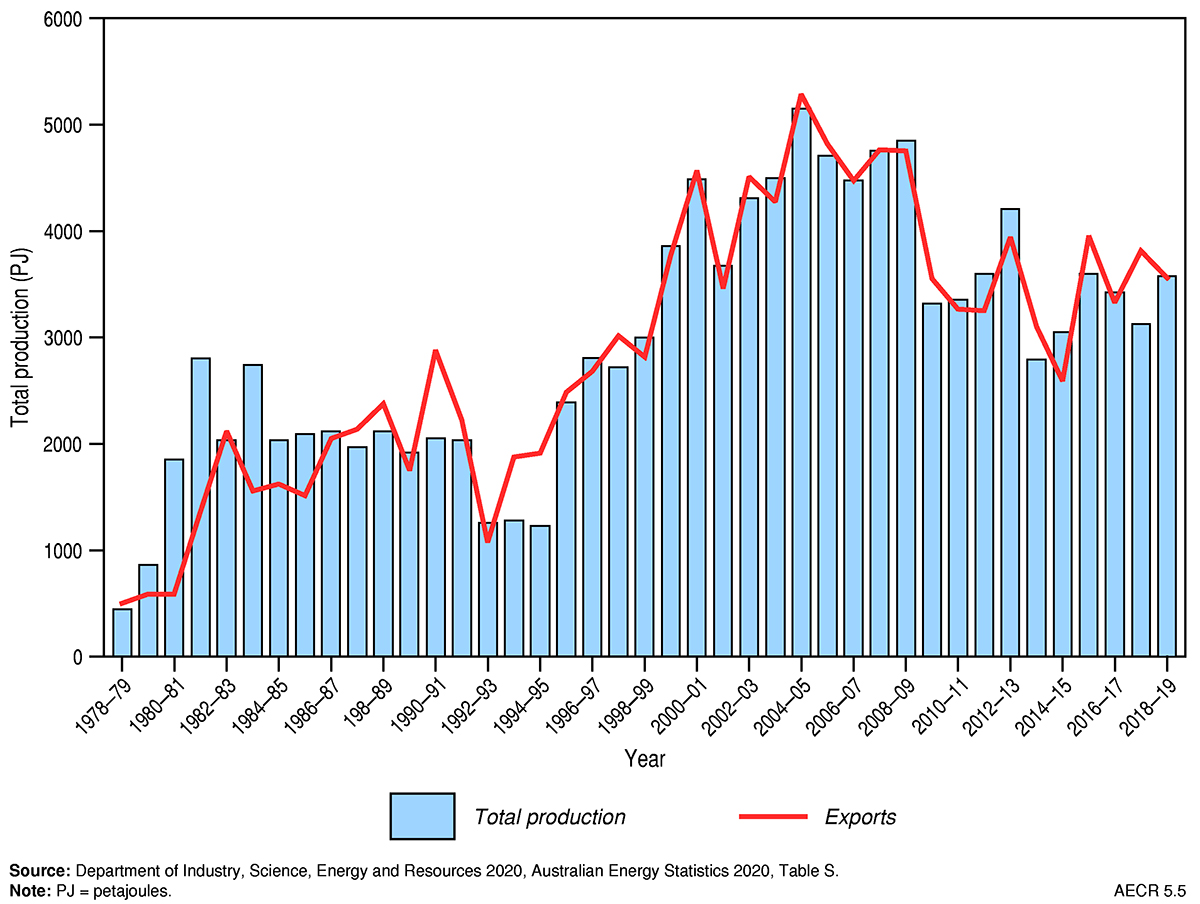

Australia is the world’s third largest uranium producer after Kazakhstan and Canada. In 2019, Australia’s production of uranium was approximately 6,613 ktU (3,703 PJ; Figure 5) which is very similar to production in 2018. In 2019, Australia’s uranium production was from three operating uranium mines: Olympic Dam and Four Mile in South Australia, and Ranger in the Northern Territory (Figure 6). Australian uranium production will fall by about 30 per cent (approximately 1900 tU p.a.) in the short to medium term due to the cessation of mining at the Ranger mine. All of Australia’s domestic production is exported.

As of January 2021, new mining is proposed at Boss Energy’s Honeymoon project (South Australia). In Western Australia, the Cameco Australia’s Kintyre and Yeelirrie projects, Toro Energy’s Wiluna project, and Vimy Resources Mulga Rock project have all received environmental approval (Figure 6). Development of these projects is contingent on international uranium market conditions.

Global uranium production is focused in a small number of countries, with Australia, Kazakhstan, Canada, Namibia, South Africa and Niger accounting for most production. Proterozoic unconformity-related deposits in Canada dominate the categories of lowest production cost. The sandstone-hosted resources of Kazakhstan, Niger and the United States comprise the next cost level. The Australian Olympic Dam breccia complex deposit is dominant in the key cost category of less than US$130/kgU.

Trade

Australia exports all its uranium production to countries within its network of bilateral safeguards agreements, which now total 43. These agreements ensure that Australian uranium is only used for peaceful purposes and does not contribute to any military applications. Australian mining companies supply uranium under long-term contracts to electricity utilities in North America, Europe and Asia. In 2019, Australia exported 3,875 PJ (6,919 ktU), which was a 20 per cent increase compared to the previous year.

World resources

The Organisation for Economic Co-operation and Development Nuclear Energy Agency and the International Atomic Energy Agency (OECD NEA and IAEA) describe 15 uranium deposit types. The largest tonnages are the sandstone, Proterozoic unconformity and Polymetallic iron-oxide breccia complex deposits (OECD-NEA and IAEA, 2020).

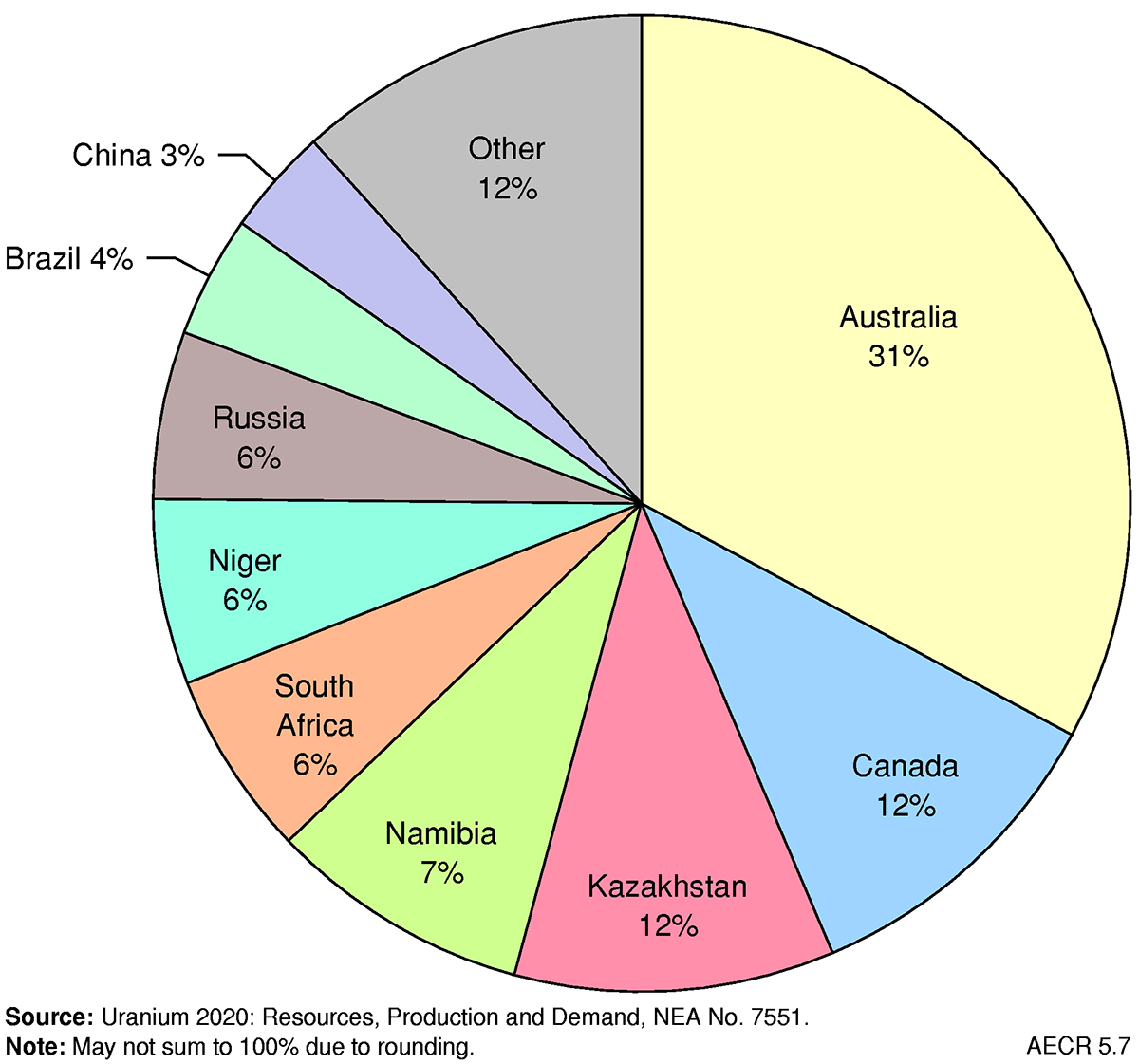

World Reasonably Assured Resources (RAR) of uranium recoverable at less than US$130/kgU were estimated at approximately 3,791 million tonnes (Mt) in 2020 (OECD NEA and IAEA, 2020). Australia accounts for approximately 31 per cent of this global inventory (Figure 7) (Table 1).

Extracting the latent energy value of thorium in a cost-effective manner is a challenge and requires considerable investment in research and development (World Nuclear Association, 2017). Another challenge is that thorium can only be used as a fuel in conjunction with a fissile material such as recycled plutonium.

Thorium-fuelled reactors have previously operated to generate electricity at Hamm-Uentrop in Germany (300 MWe, 1983–1989), at Peach Bottom (40 MWe, 1967–1974), Fort St Vrain (330 MWe, 1976–1989) and Shippingport (60 MWe, 1977–1982) in the United States (World Nuclear Association, 2017), with India having a longstanding program to develop thorium-based reactors. India has one small test facility in operation with a network of larger commercial facilities planned (World Nuclear Association, 2019; Power, 2019).

However, as international research into associated technologies tends to be small scale and intermittent (e.g. New Scientist, 2017), commercial use of thorium as a nuclear reactor fuel is still some decades away.

Table 1. Key uranium statistics

| Unit | Australia 2018 | Australia 2019 | OECD 2018 | World 2018 | |

|---|---|---|---|---|---|

| Resources | |||||

| Identified RAR recoverable at <US$130/kg U | t U | 1,183,900 | na | 1,749,200 | 3,791,700 |

| Share of World | % | 31.0 | na | 46.0 | 100 |

| World Ranking | 1 | na | na | na | |

| Production | |||||

| Annual production | PJ | 3,655 | 3,703 | 7,749 | 29,969 |

| t U | 6,526 | 6,613 | 13,838 | 53,516 | |

| Share of world | % | 12.2 | na | 25.9 | 100 |

| World ranking | no. | 3 | 3 | 2 | na |

| CAGR from 2009 | % | na | -2.9 | na | na |

| Exports | |||||

| Annual exports | PJ | 3,235 | 3,875 | na | na |

| t U | 5,776 | 6,919 | na | na | |

| Export value | A$b | 0.6 | 0.7 | na | na |

Notes: t = tonne. PJ = petajoule. RAR = Reasonably Assured Resources. CAGR = compound annual growth rate. OECD = Organisation for Economic Co-operation and Development countries. na = not available or not applicable. Source: Resources and production data from OECD NEA and IAEA (2020) Uranium 2020: Resources, Production and Demand, NEA No. 7551; export data from Department of Industry, Science, Energy and Resources (2020) Resources and Energy Quarterly, December 2020.

References

Department of Industry, Science, Energy and Resources 2020. Resources and Energy Quarterly, December 2020 (last accessed 27 April 2021).

New Scientist 2017. Thorium could power the next generation of nuclear reactors (last accessed 28 April 2021).

Organisation for Economic Co-operation and Development Nuclear Energy Agency and International Atomic Energy Agency (OECD NEA and IAEA) 2020. Uranium 2020: Resources, Production and Demand (last accessed 27 April 2021).

Power 2019. Indian-designed nuclear reactor breaks record for continuous operation (last accessed 28 April 2021).

World Nuclear Association 2017. Thorium (last accessed 28 April 2021).

World Nuclear Association 2019. Nuclear Power in India (last accessed 28 April 2021).

Data download

Australia’s Energy Commodity Resources: 2018 and 2019 Data Tables.